Summary

Keywords

Full Transcript

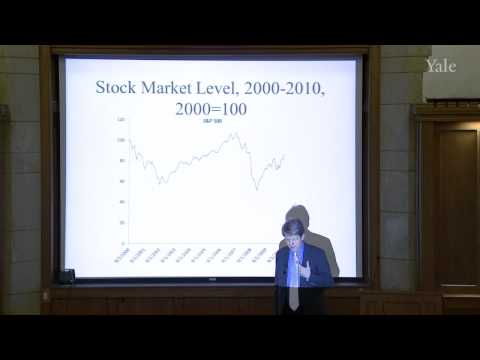

Financial Markets (2011) (ECON 252) Professor Shiller introduces basic concepts from probability theory and embeds these concepts into the concrete context of financial crises, with examples from the financial crisis from 2007-2008. Subsequent to a historical narrative of the financial crisis from 2007-2008, he turns to the definition of the expected value and the variance of a random variable, as well as the covariance and the correlation of two random variables. The concept of independence leads to the law of large numbers, but financial crises show that the assumption of independence can be deceiving, in particular through its impact on the computation of Value at Risk measures. Moreover, he covers regression analysis for financial returns, which leads to the decomposition of a financial asset's risk into idiosyncratic and systematic risk. Professor Shiller concludes by talking about the prominent assumption that random shocks to the financial economy are normally distributed. Historical stock market patterns, specifically during crises times, establish that outliers occur too frequently to be compatible with the normal distribution. 00:00 - Chapter 1. Financial Crisis of 2007-2008 and Its Connection to Probability Theory 05:51 - Chapter 2. Introduction to Probability Theory 09:58 - Chapter 3. Financial Return and Basic Statistical Concepts 26:29 - Chapter 4. Independence and Failure of Independence as a Cause for Financial Crises 38:58 - Chapter 5. Regression Analysis, Systematic vs. Idiosyncratic Risk 58:59 - Chapter 6. Fat-Tailed Distributions and their Role during Financial Crises Complete course materials are available at the Yale Online website: online.yale.edu This course was recorded in Spring 2011.

Continue this lesson in the app

Install CourseHive on Android or iOS to keep learning while you move.